Life’s unexpected turns can transform stability into uncertainty in an instant. Perhaps a career shift altered monthly income, a medical setback reshaped priorities, or a former partner’s circumstances evolved dramatically.

Each scenario leaves lasting ripples, making outdated support arrangements feel heavy, unfair, or unsustainable. In Rolling Meadows, every petition to amend spousal maintenance carries deeply personal stakes—financial security, dignity, and peace of mind.

Navigating complex Cook County procedures independently can lead to frustration, costly delays, and missed opportunities. You deserve more than generic advice; you deserve a trusted ally who listens, strategizes, and acts decisively on your behalf.

At Cooper Trachtenberg Law Group, we understand the weight of these moments and the urgency to restore balance.

Our tailored approach combines local insight, precise legal action, and compassionate guidance, ensuring your future reflects your current reality. Change isn’t easy, but with the right advocate, it’s possible—and it starts here.

What Spousal Maintenance Modification Means in Illinois

An outdated support order can feel like a chain holding you back, draining your finances, limiting your freedom, and ignoring the reality of your current life. Illinois law gives you the chance to change that.

A spousal maintenance modification isn’t just a legal process; it’s your opportunity to realign the terms with your current life, whether that means easing an unbearable payment or increasing the support you need to stay afloat.

Every month that passes without change is money lost and stress gained.

Why Local Knowledge Matters in Rolling Meadows and Family Court

Walking into Family Court without someone who knows the terrain is like stepping into a maze blindfolded. Rules are one thing—how they’re applied here is another. Judges have preferences.

Clerks have quirks. Deadlines aren’t forgiving. One missed detail could cost you months, even years, of relief.

You need someone who not only understands Illinois law but can navigate the Rolling Meadows courthouse like second nature—protecting your time, your money, and your future.

2025 Updates Impacting Modification Cases in Cook County

If you’re counting on old rules to protect you, you’re already at risk. In 2025, Cook County cases will face stricter requirements, including no more automatic pauses on payments during incarceration, new income review standards, and zero tolerance for incomplete filings.

These changes can bury your request before it’s even heard unless your attorney knows exactly how to position it.

Falling behind isn’t just about numbers—it’s about sleepless nights, strained budgets, and the constant weight of uncertainty.

If your current spousal maintenance order no longer reflects your reality, Cooper Trachtenberg Law Group can help you seek a fair adjustment. Contact us today to begin your case.

If you’re ready to get started, call us now!

When a Spousal Maintenance Order Can Be Changed

Not every change in life qualifies for a new support order, but when it does, acting quickly can protect your finances and your peace of mind.

Here’s how the law decides whether your circumstances warrant an update.

Recognizing Substantial Changes in Circumstances

Life doesn’t stand still, and neither should your support order. Illinois courts allow changes when your reality has shifted in a meaningful way—changes that make your current agreement unfair or impossible to maintain.

These aren’t minor inconveniences; they’re turning points that deserve legal recognition before they drain your savings or disrupt your stability.

Income Changes, Job Loss, or Retirement

A sudden layoff. A forced reduction in hours. The decision to retire after decades of work. Any of these can throw your budget into chaos if your spousal maintenance order doesn’t adapt.

Without an adjustment, you could find yourself falling behind on bills or losing the financial footing you’ve worked so hard to build.

We make sure the court understands your situation before the damage becomes permanent.

Remarriage or Cohabitation Impact on Support

If your former spouse remarries or begins living in a marriage-like relationship, the law may allow you to stop payments entirely.

However, nothing changes automatically—you must take action to protect your rights. Waiting means money out of your pocket every month that should be staying with you.

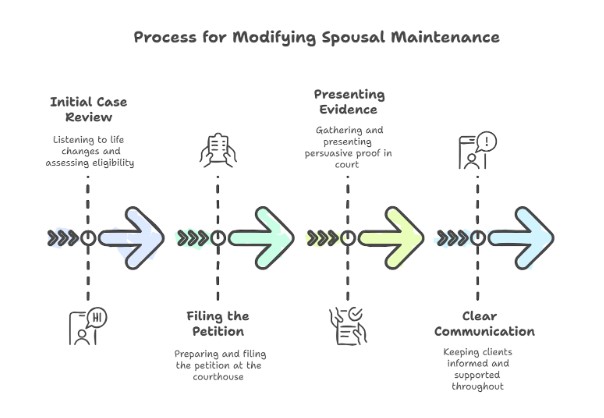

Our Process for Modifying Spousal Maintenance in Rolling Meadows

We’ve built our approach to provide you with clarity, speed, and confidence at every step, so you always know exactly where your case stands and what’s next.

Initial Case Review and Eligibility Assessment

We start by listening—listening—to what’s changed in your life. Then we evaluate whether those changes meet the court’s standard for a modification.

You’ll know exactly where you stand before you invest time or money.

Filing the Petition at the Courthouse

We prepare your petition with precision, file it at the courthouse, and ensure every form, signature, and deadline is met. No oversights. No costly delays.

Presenting Evidence and Court Representation

Your story needs more than paperwork—it needs persuasive proof. We gather the documents, financial records, and witness statements that bring your situation into sharp focus for the judge, then stand beside you every step of the way.

Clear Communication from Start to Finish

You’ll never be left wondering what’s happening with your case. We keep you updated, explain each decision point, and respond promptly so you feel supported, informed, and in control throughout the process.

Understanding Illinois Maintenance Guidelines

Before you can change your spousal maintenance order, you need to understand how Illinois determines what’s fair.

These guidelines aren’t just numbers—they’re the framework judges use to shape your financial future.

Formula for Calculating Modified Support

Illinois uses a set formula: 33⅓% % of the payer’s net income minus 25% of the recipient’s, capped at 40% of combined net income.

While the math seems straightforward, the real work lies in accurately documenting income, deductions, and any special circumstances that could influence the outcome.

Duration Adjustments Based on Marriage Length

The longer the marriage, the longer maintenance may last. Illinois assigns duration multipliers based on the number of years you were married, meaning even small differences in calculated marriage length can significantly change how long payments continue.

Court Discretion and Exceptions

Judges aren’t bound to the formula in every case. Health concerns, disability, drastic life changes, or unique financial arrangements can justify a departure from the guidelines. Knowing when and how to present these factors is critical.

Changes in income, health, or family status can’t wait. Cooper Trachtenberg Law Group will guide your Rolling Meadows modification from petition to resolution—schedule your consultation now.

If you’re ready to get started, call us now!

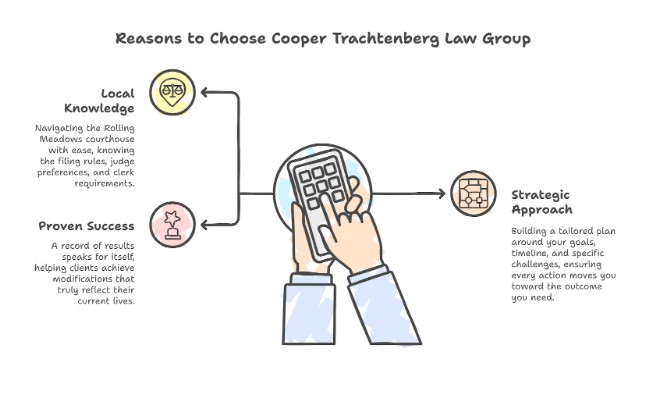

Why Choose Cooper Trachtenberg Law Group in Rolling Meadows

When you’re seeking a modification, who represents you matters as much as the law itself.

Here’s why families in Rolling Meadows trust us to fight for fair, lasting results.

Local Knowledge of Cook County Family Court Procedures

We navigate the Rolling Meadows courthouse with ease, knowing the filing rules, judge preferences, and clerk requirements that can make or break a case.

This insider understanding helps us avoid delays and anticipate challenges.

Strategic, Client-Focused Legal Approach

Your case isn’t just another file to us. We build a tailored plan around your goals, your timeline, and your specific challenges—ensuring every action we take moves you toward the outcome you need.

Proven Success in Support Modification Cases

From reducing unfair obligations to increasing necessary support, our record of results speaks for itself.

We’ve helped clients in situations just like yours achieve modifications that truly reflect their current lives.

Rolling Meadows Family Court Information

Knowing where and how to file can save you hours of frustration. Here’s the practical information you’ll need when pursuing your modification in Rolling Meadows.

Rolling Meadows Courthouse Address and Contact Details

Rolling Meadows Courthouse

2121 Euclid Avenue, Rolling Meadows, IL 60008

Phone: (847) 818-3000

Parking and Public Transportation Access

Ample on-site parking is available, with designated spaces for visitors. Public transportation options include nearby bus routes and Metra service, offering convenient access from surrounding suburbs.

Filing Hours and Local Clerk Information

The Clerk’s Office is typically open Monday through Friday, 8:30 a.m. to 4:30 p.m., excluding holidays. Arriving early can help you avoid lines and ensure same-day processing.

Our Related Services – Illinois Family Law and Real Estate Attorneys

At Cooper Trachtenberg Law Group, our work extends beyond spousal maintenance modifications.

With more than 30 years of combined experience, we provide Rolling Meadows, Illinois families and property owners with trusted legal support in life’s most important transitions.

Our primary services include:

- Divorce Representation – Guiding clients through every stage of divorce, from filing to final decree, with a focus on protecting assets, children, and peace of mind.

- Child Support & Parenting Matters – Securing fair support arrangements and workable parenting schedules that put children’s needs first.

- Mediation Services – Offering a private, less adversarial path to resolving family disputes without lengthy court battles.

- Real Estate Law – Handling property sales, purchases, leases, development, zoning, and foreclosure defense across Illinois.

Each service is approached with professionalism, discretion, and a commitment to achieving the best possible outcome for every client.

Stop letting an outdated support order strain your finances. Cooper Trachtenberg Law Group is ready to fight for terms that match your life today. Contact us to get started.

Contact Us Today For An Appointment

Frequently Asked Questions

When can I request a spousal maintenance modification in Illinois?

You can request a change if there’s a substantial shift in circumstances—such as income changes, job loss, retirement, health issues, remarriage, or cohabitation.

Does the court automatically adjust support if my ex remarries?

No. Even if remarriage or cohabitation qualifies for termination, you must file a formal petition with the court to stop payments.

How long does it take to modify spousal maintenance in Rolling Meadows?

Most cases take several months, depending on court scheduling, complexity, and whether the request is contested.

Will the judge use the same formula for modified support?

Yes, Illinois applies a statutory formula for calculating maintenance, but the court may deviate for fairness or special circumstances.

What documents should I bring to my attorney?

Bring recent tax returns, pay stubs, proof of expenses, medical records (if relevant), and any evidence supporting your claim for modification.

Can my maintenance be reduced if I retire?

Yes, if retirement significantly impacts your income and ability to pay, the court may lower or terminate the obligation.

Do I need an attorney to file for modification?

While not legally required, having an attorney increases your chances of success by ensuring proper filing, evidence gathering, and representation in court.