Data last verified: March 2026

Illinois divorce courts require financial transparency because child support, maintenance, and property division all depend on verified income figures.

When a spouse conceals pay, underreports business revenue, or hides cash income, Illinois law provides multiple overlapping tools to force disclosure — and those tools can run in parallel, not in a rigid sequence.

Illinois judges can order a non-disclosing spouse to produce income records, comply with written discovery, and respond to subpoenas.

Illinois judges can also impose discovery sanctions under Illinois Supreme Court Rule 219 when a spouse refuses to comply with court orders.

Illinois divorce financial disclosure supports accurate child support, maintenance, attorney fee allocation, and equitable property division. Illinois judges cannot evaluate cash flow, earning capacity, or marital estate structure without reliable income records, because income affects both ongoing payment obligations and settlement leverage.

Illinois law requires a standardized financial affidavit in divorce and family cases, supported by tax returns, pay stubs, and banking statements under750 ILCS 5/501(a)(1).

A sworn financial affidavit creates a legal record because a party signs it under oath, making incomplete or false disclosure a serious exposure point.

Illinois divorce “income” often exceeds taxable wages. Illinois support analysis can include bonuses, commissions, self-employment draws, investment distributions, and other recurring compensation streams when the evidence supports the classification. Cases involving high-conflict divorce dynamics often surface the most aggressive income concealment patterns.

A spouse who wants to translate income findings into a workable settlement plan often benefits from structured divorce financial planning from the start.

If you’re ready to get started, call us now!

The requesting party’s tender of their own Financial Affidavit with supporting documents to the other party is the triggering event for all income disclosure tools.

Once that affidavit is tendered, the requesting party can issue written discovery, serve third-party subpoenas, serve notice of depositions, and retain experts — and none of these tools requires that the others be completed first.

Illinois courts expect both parties to meet the same disclosure baseline. Under Cook County Court Rule 13.3.1, the petitioner must serve a completed Financial Affidavit no later than 30 days after service of the initial pleading, and the respondent must do the same within 30 days of filing an appearance.

A spouse who withholds income records after the other side has tendered full disclosure creates a court record that supports sanctions, fee shifting, and other remedial orders.

Cases involving business ownership, self-employment, or complex compensation structures often benefit from divorce discovery tools deployed simultaneously from the start of the case.

Illinois divorce discovery does not follow a mandatory linear sequence. The tools below can be used in parallel and in any combination that the facts of the case require.

Interrogatories force sworn written answers about employment history, compensation structure, side income, business interests, and account locations under Illinois Supreme Court Rule 213.

Requests for production compel the delivery of documents, including electronically stored information, under Illinois Supreme Court Rule 214. Illinois written discovery commonly runs on a 28-day response window unless a court order adjusts the schedule.

A spouse who receives evasive or partial answers should treat incomplete disclosure as a compliance problem that requires escalation, not a negotiation issue to resolve informally.

A third-party subpoena can be served at any time after the requesting party tenders their Financial Affidavit — it does not need to wait for written discovery to be issued or to go unanswered.

Subpoenas under Illinois Supreme Court Rule 204 pull records directly from employers, banks, investment platforms, and tax preparers, bypassing the non-disclosing spouse entirely.

Third-party documents carry independent business-record reliability, which typically makes them stronger evidence than self-reported disclosure.

Cook County practitioners can review the county-specific process for financial subpoenas in Cook County divorce cases; DuPage County cases follow related procedures under DuPage County discovery.

Depositions allow sworn oral testimony from the opposing spouse, employers, business partners, accountants, bookkeepers, and other third parties with knowledge of income and assets.

Deposition testimony creates a record that is difficult to walk back and frequently surfaces inconsistencies between a spouse’s sworn affidavit statements and third-party documents. Illinois Supreme Court Rule 206 governs deposition procedures in divorce cases.

Income concealment tied to business ownership, self-employment, or complex compensation structures often requires expert analysis to reconstruct and present clearly to the court.

Forensic accountants can rebuild income from bank deposits, business records, and lifestyle spending patterns.

Valuators assess business interests and asset values that affect both support calculations and equitable division.

Experts can also identify cash flow manipulation and hidden assets that standard written discovery does not surface on its own. The Illinois CPA Society maintains a directory of forensic accounting professionals with family law experience.

A spouse who ignores or evades discovery after it is properly issued triggers an enforcement sequence. Illinois practice under Illinois Supreme Court Rule 201(k) requires attorneys to make a good-faith effort to resolve discovery disputes before filing a motion to compel.

That effort includes completing a mandatory 201(k) conference — a direct attorney-to-attorney communication that must occur after discovery is past due and before seeking court intervention.

If the 201(k) conference does not resolve the dispute, the requesting party can file a motion to compel. A strong motion to compel package includes the original discovery requests, the deficiency notice, documentation of the 201(k) conference, and a clear itemized list of missing items with dates.

Illinois judges often issue compliance orders with explicit deadlines and follow-up status dates to evaluate whether a spouse is acting in good faith.

A spouse who ignores a court order creates an enforcement posture that invites escalating consequences. A spouse who wants a plain-language explanation of what order violations entail can review the consequences of court order violations in Illinois divorce.

When income records stay missing, Cooper Trachtenberg Law Group can escalate from written discovery to subpoenas, depositions, and motions to compel. Contact us today.

If you’re ready to get started, call us now!

Illinois discovery sanctions exist to correct unfairness and deter noncompliance, not simply to punish. Illinois Supreme Court Rule 219(c) is designed to coerce compliance with discovery rules and orders, and courts must strike a balance between enforcing discovery rules and resolving cases on the merits.

Illinois judges can order fee shifting when one spouse’s obstruction drives unnecessary motion practice.

Illinois Supreme Court Rules 137 and 219(c) allow for attorney fees and monetary penalties when the court finds sanctionable conduct by another party or attorney.

Illinois judges can also restrict the use of evidence, strike pleadings, or enter other remedial orders designed to prevent a spouse from benefiting from nondisclosure, depending on the procedural posture and the record.

Illinois financial affidavits carry special risk because 750 ILCS 5/501(a)(1) requires the financial affidavit to be supported by documentary evidence, including income tax returns, pay stubs, and banking statements.

A spouse who submits an incomplete affidavit often triggers deeper discovery because the gaps in the affidavit serve as a roadmap to what is missing.

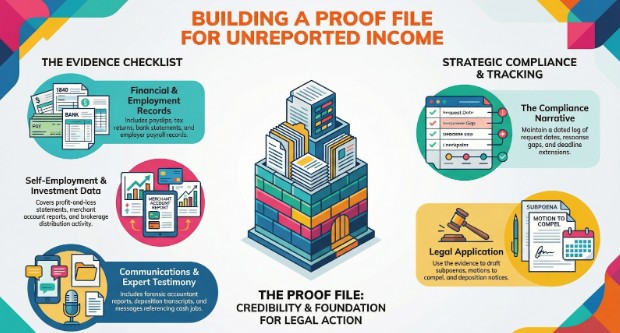

A proof file wins credibility because it lets the judge see a pattern. A proof file also provides counsel with the information needed to draft subpoenas, motions to compel, deposition notices, and targeted expert-retention letters.

A spouse improves court outcomes by documenting request dates, response gaps, and follow-up steps, as this documentation supports a clear compliance narrative for the judge.

A spouse who expects settlement talks can also pair the proof file with a mediation preparation posture that uses defined income categories and verified timelines.

Illinois divorce discovery timelines vary by county, judge, and case complexity. The table below reflects the corrected framework — tools run in parallel after the Financial Affidavit is tendered, not in a mandatory sequence.

| Stage | Tool | What Gets Served Or Filed | Typical Response Window | Decision Trigger |

| 1 | Financial Affidavit tender | The requesting party serves its own affidavit with supporting documents | 30 days after initial pleading (Cook County Rule 13.3.1) | Activates all discovery rights |

| 2 | Written discovery | Interrogatories under Rule 213; RFP under Rule 214 | Often 28 days unless ordered otherwise | Evasive answers, missing sources, incomplete documents |

| 3 | Third-party subpoenas | Records from employers, banks, tax preparers under Rule 204 | Varies by recipient | Available any time after affidavit tender; bypasses spouse entirely |

| 4 | Depositions | Sworn oral testimony of spouse or third parties under Rule 206 | Scheduled by notice | Inconsistencies between affidavit and third-party records |

| 5 | Expert retention | Forensic accountant, valuator, or other specialist | Ongoing | Complex income, business interests, or suspected hidden assets |

| 6 | 201(k) conference | Mandatory good-faith attorney conference after discovery is past due | Before motion to compel | Required prerequisite before court intervention |

| 7 | Motion to compel | Court motion with deficiency list and 201(k) documentation | Hearing set by court | Nonresponse after written discovery and 201(k) conference |

| 8 | Sanctions | Rule 219 remedies request | Court-specific | Continued noncompliance after court order |

A spouse who needs a faster path should prioritize third-party subpoenas and expert retention when payroll, bank, and business records exist outside the spouse’s direct control.

If nondisclosure is delaying your divorce, request a strategy call with Cooper Trachtenberg Law Group to build proof, enforce orders, and move forward. Contact us.

What can I do first if my spouse won’t disclose income in an Illinois divorce?

The first step is to tender your own Financial Affidavit, with supporting documents, to the other party. That tender activates your right to issue written discovery, serve third-party subpoenas, notice depositions, and retain experts — all simultaneously.

Can an Illinois judge force my spouse to provide pay stubs and tax returns?

Illinois judges can order the production of income documents through discovery orders. Sanctions under Illinois Supreme Court Rule 219 apply when a spouse disobeys discovery rules or court orders and may include fee shifting, evidentiary restrictions, and other remedial orders.

What discovery requests work best for hidden income?

Written discovery under Illinois Supreme Court Rule 213 and Rule 214 targets income sources and supporting documents. Third-party subpoenas under Rule 204 compel employers and banks to produce records directly. Depositions and forensic accountant analysis are also effective when income concealment involves business ownership, self-employment, or complex compensation structures.

Can I subpoena my spouse’s employer or bank before written discovery is complete?

Yes. A third-party subpoena under Illinois Supreme Court Rule 204 can be served at any time after the requesting party tenders its Financial Affidavit with supporting documents. Subpoenas do not need to wait for written discovery to be issued or to go unanswered.

What is a 201(k) conference, and when does it happen?

A 201(k) conference is a mandatory good-faith attorney communication required before a party can file a motion to compel. It occurs after discovery has been issued, and the response deadline has passed without adequate compliance, not before discovery is served.

What happens if my spouse lies on a financial affidavit?

Illinois requires a statewide financial affidavit, along with supporting documents, under 750 ILCS 5/501. A false or incomplete affidavit can trigger deeper written discovery, third-party subpoenas, depositions, expert analysis, and potential sanctions depending on the record.

How long does it take to force income disclosure in an Illinois divorce?

Timing depends on county scheduling, case complexity, and compliance. Many cases move from written discovery to subpoenas and depositions within weeks, then escalate to a motion to compel and sanctions if a spouse continues refusing. Third-party subpoenas often produce records faster than waiting for a spouse to comply directly.

About the Author

Partner · Fellow, American Academy of Matrimonial Lawyers (AAML) · Illinois Family Law Attorney · Mediator · Collaborative Divorce Practitioner

Helena L. Trachtenberg is a Partner at Cooper Trachtenberg Law Group, LLC and a Fellow of the American Academy of Matrimonial Lawyers (AAML), an invitation-only organization that recognizes the nation's leading family law attorneys.

Her practice is devoted exclusively to Illinois family law matters, including divorce, allocation of parental responsibilities, parenting time, child support, property division, prenuptial agreements, post-decree litigation, and complex family law disputes throughout the Chicago area.

Helena is a trained mediator, collaborative law practitioner, Child Representative, Guardian ad Litem, and Parenting Coordinator. She also has extensive experience handling matters involving the Illinois Department of Children and Family Services (DCFS) and the Illinois Department of Healthcare and Family Services (HFS).

Through litigation, mediation, and collaborative law, Helena helps clients navigate challenging family transitions while pursuing practical and effective resolutions that protect their long-term interests.

Practice Areas: Divorce, Collaborative Divorce, Mediation, Child Custody, Parenting Time, Child Support, Property Division, Prenuptial Agreements, Post-Decree Matters

Practice Areas

Legal Support When You Need It Most

Testimonials

Main Office

3601 Algonquin Road, Suite 610

Rolling Meadows, Illinois 60008

Lincolnshire Office

250 Parkway Drive, Suite 150

Lincolnshire, IL 60069

By Appointment Only

Phone:

847-995-8800

We represent parties across the Chicago area, including Arlington Heights, Barrington, Buffalo Grove, Carol Stream, Evanston, Glenview, Highland Park, Hinsdale, Inverness, Lincolnshire, Long Grove, Mt. Prospect, Palatine, Rolling Meadows, Schaumburg, Skokie, Streamwood, Wheeling and more. We also represent clients from Cook, Lake, DuPage, Kane and McHenry counties.

© 2026 by Cooper Trachtenberg Law Group, LLC. All Rights Reserved.

Disclaimer |

Site Map